Health Insurance Explained

What Is Health Insurance?

Health insurance is a contract designed to help cover the cost of medical care. When you enroll in a health insurance plan, you agree to pay a monthly premium. In return, your insurer pays part of your healthcare expenses, providing valuable financial protection and access to medical services.

What Does Health Insurance Cover?

· Doctor visits

· Hospital stays

· Prescription medications

· Preventive care, such as vaccines and screenings

Benefits of Health Insurance

By having health insurance, you are protected from high out-of-pocket costs that can arise from unexpected medical needs. Additionally, health insurance ensures that you can access timely medical services, helping you maintain your health and well-being.

Financial Risks

Without health insurance, individuals face significant financial burdens. High out-of-pocket costs mean that you are responsible for the entire expense of medical services, including hospital stays, surgeries, prescriptions, and emergency care. For example, a single emergency room visit can amount to thousands of dollars. This financial strain often leads to medical debt, with more than 60% of uninsured Americans reporting that they have incurred debt due to medical expenses they could not afford. Additionally, uninsured individuals do not benefit from the discounted rates that insurance companies negotiate for their members. As a result, those without insurance typically pay much more for the same medical services than insured patients.

Health Consequences

Lack of health insurance often results in delayed or skipped medical care because of cost concerns.

Many uninsured people avoid seeking medical attention, which can cause health conditions to worsen or lead to complications that might have been preventable with timely care. Furthermore, without insurance, routine checkups, screenings, and vaccinations are frequently neglected, making it more likely for illnesses to go undetected. Research shows that uninsured individuals are at a higher risk of suffering from preventable or treatable conditions due to a lack of timely medical intervention, which can ultimately lead to a greater risk of mortality.

Legal and Regional Penalties

While the federal requirement to carry health insurance was removed in 2019, some states still mandate that residents obtain coverage. States such as California, Massachusetts, New Jersey, Rhode Island, and Washington D.C. have established their own health insurance requirements and impose penalties on residents who do not comply.

There are several types of health insurance, which we will review next.

Types of Health Insurances

Private Health Insurance

Private health insurance is offered by companies such as Blue Cross, UnitedHealthcare, and Aetna. Individuals can purchase these plans directly or receive them through an employer. Coverage, premiums, and provider networks may differ significantly between plans.

Employer-Sponsored Insurance (ESI)

Many employers provide health insurance as part of employee benefits. These plans often include group discounts and shared premium costs, and may offer various options such as Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and High-Deductible Health Plans (HDHPs).

Government-Sponsored Insurance

· Medicare: Available to individuals aged 65 or older and people with certain disabilities. It includes:

· Part A: Hospital insurance

· Part B: Medical insurance

· Part C: Medicare Advantage (private plans)

· Part D: Prescription drug coverage

Medicaid: Designed for low-income individuals and families. Eligibility and benefits vary by state, but it generally covers a wide range of services at little to no cost.

CHIP (Children’s Health Insurance Program): Provides coverage for children in families earning too much for Medicaid but unable to afford private insurance. CHIP is state-administered under federal guidelines.

Marketplace Plans (ACA)

Marketplace plans are purchased through the Health Insurance Marketplace, either on Healthcare.gov or a state exchange. These plans are categorized by metal tiers: Bronze, Silver, Gold, and Platinum. Depending on income, subsidies are available to help reduce premium costs.

Short-Term Health Insurance

Short-term health insurance offers temporary coverage for situations such as gaps between jobs. These plans typically have lower premiums but provide limited benefits and may exclude coverage for pre-existing conditions. They are not compliant with the Affordable Care Act (ACA).

High-Deductible Health Plans (HDHP)

HDHPs feature lower monthly premiums and higher deductibles. They are often paired with Health Savings Accounts (HSAs), making them a good option for healthy individuals who want to save on premiums and set aside money for future healthcare expenses.

Catastrophic Health Insurance

Catastrophic health insurance is available to individuals under 30 or those who qualify for hardship exemptions. These plans have very low premiums and very high deductibles, covering essential health benefits only after the deductible is met.

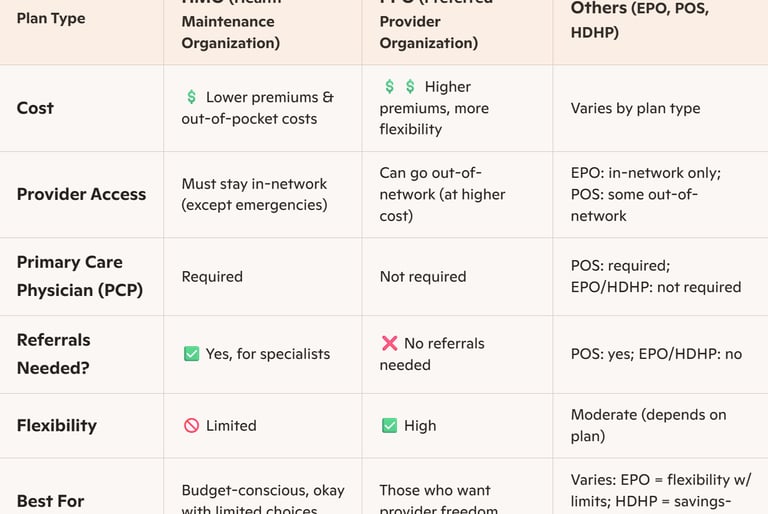

Comparing HMO and PPO Plans

Health Maintenance Organization (HMO) and Preferred Provider Organization (PPO) plans are among the most widely chosen health insurance options. Each presents different advantages and drawbacks, particularly in terms of cost, provider flexibility, and access, which can greatly influence your overall healthcare experience and financial obligations.

You didn’t come this far to stop